S&P's Top 10 key themes to the 2024 energy outlook

Analysts at S&P Global Commodity Insights, the leading independent provider of information, data, analysis, benchmark prices and workflow solutions for the commodities, energy and energy transition markets, have released their latest 2024 energy outlook.

"The still young decade has seen more than its fair share of black swan events, from the COVID pandemic to wars in Ukraine and now Gaza," explains Dan Klein, Head of Energy Pathways, S&P Global Commodity Insights. "Even if such chaotic events fail to emerge over the next 12 months, volatility will remain high as most energy markets have not yet been able to adapt to previous swings in supply and demand fundamentals to find a new normal."

Energy demand searching for a new normal but will be hard-pressed to find it.

Once fairly steady due to relatively predictable economic and population growth, energy demand has been subject to unprecedented volatility since the new decade began. From the staggering level of demand destruction from the COVID pandemic and the uneven geographic and sectoral recovery from it, to the repercussions of the Russian invasion of Ukraine, market participants may be wondering what "normal" demand growth looks like. The delayed recoveries from COVID in China and in the aviation sector are now essentially complete and markets have generally adjusted to altered flows of Russian energy, but there still are several wildcards for demand in 2024:

- Central banks face the continued challenge of reining in inflation without damaging economic growth.

- China's economic slowdown could cause ripples across the region and the globe.

- Questions remain around the recovery of European power and gas demand, approaching two years since the start of the Ukraine conflict.

- 2024 will be an El Niño year, with a 30% chance that the weather phenomenon could be historically intense. Against a background of rising global temperatures, a strong El Niño could drive extreme weather on both sides of the Pacific (and beyond), amplifying swings in energy demand and increasing the likelihood of a more active hurricane season.

Coal demand likely peaked in 2023; global consumption to start declining in 2024.

Growth in renewables and other clean technology grabbed the headlines in 2023, but the use of coal quietly grew in the background, with consumption likely hitting a new annual record in 2023. The strength in global demand was driven by China's delayed economic recovery from COVID combined with underperforming hydro generation. In 2024, an expected rebound in Chinese hydro generation, a continued renewables build-out, and slower electricity load growth should see Chinese coal demand growth decelerate notably from 2023 levels. Coal demand will assuredly grow in India and other developing nations in 2024, but with weaker Chinese coal growth, the continued structural decline in demand in the US, Europe, and other industrialised nations, global demand very likely has peaked. However, coal often is the fuel to backfill for underperforming renewables, when natural gas is too expensive or unavailable and if overall energy demand is higher than anticipated. As a result, another year or two of growth is not completely out of the question.

One in five cars sold in 2024 will be electric, putting global gasoline demand on the edge of its peak.

Sales of electric vehicles (EVs) have surged over the past several years, stimulated by subsidies and tax incentives. However, EVs have become cost competitive in some markets without subsidies and automakers are offering a significantly larger and more diverse portfolio of new EV models and sales growth is starting to hit another gear. More than a million new EVs are taking to the roads every month, and EV penetration of new vehicle sales is now over 30% in China, over 20% in Europe, and over 10% in the US. S&P Global Commodity Insights projects that EV sales penetration will reach 20% globally in 2024, fuelled by a significant increase in the US related to the Inflation Reduction Act and new models on offer. This influx of new EVs – combined with sustained improvements in the fleet ICE vehicle fuel efficiencies – will slow gasoline demand growth to less than 300,000 b/d in 2024, and that this may be the last year of global growth for the fuel.

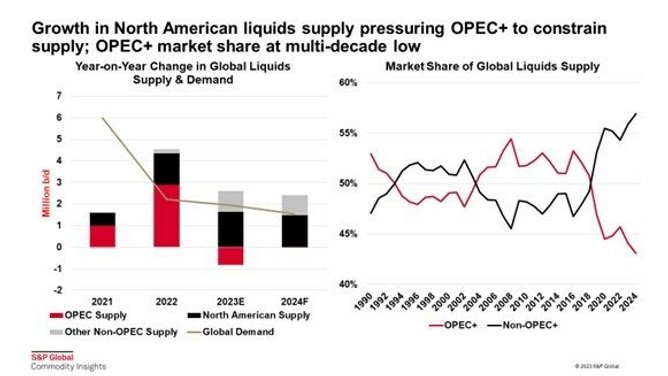

Massive growth in North American oil and natural gas supply growth to continue.

Due in large part to strong oil prices, US oil and gas production surged to new record levels in 2023. The US now produces around 22 million barrels per day (b/d) of total liquids, growing by 1.3 million b/d in 2023 alone. Even assuming weaker oil prices and a slowdown in new drilling going forward, there is sufficient momentum already in place to see nearly 1 million b/d of growth in 2024 due to increased rig efficiency and longer laterals. With Canadian liquids expanding by nearly 0.4 million b/d, North American liquids supply growth is expected – on its own – to meet over 85% of global demand growth in 2024. Despite low Henry Hub gas prices in 2023, and a pullback in gas-oriented drilling, lower-48 natural gas production will reach 103.4 billion cubic feet per day (Bcf/d) in 2024, up by 4.3 Bcf/d due to strong oil prices stimulating associated gas production. Production growth is expected to slow but remain positive in 2024, which will continue the push for higher LNG and pipeline exports.

OPEC+ and other producers in a difficult position.

Throughout 2023, faced with increasing North American liquids production as well as growth elsewhere in non-OPEC+ (Brazil, China, Norway, Mexico & Guyana), OPEC+ chose to cut production quotas in order to defend prices. While these curtailments have kept and are keeping headline crude oil prices from falling below $80/b until likely late in 2024, OPEC's market share has fallen to its lowest point in recent memory. Already, unity within OPEC+ appears to be fracturing, with members only able to agree on voluntary cuts at the delayed November 2023 meeting. OPEC+ crude production is now set to decline for the second consecutive year in 2024, even as global demand rises. Even if cuts are successful in keeping oil prices strong, this may ultimately be counterproductive as it will encourage further growth in non-OPEC+ supply (and potentially drive additional consumers to shift to EVs). There may come a point in 2024 where at least some OPEC+ members opt for a market share strategy over price defence.

A new wave of consolidation in clean tech; extended wave for fossil fuels.

The unwinding of two years of polysilicon supply constraints has resulted in lower solar project costs and potentially wider margins for developers. As a result of this shift, some companies mistimed the cycle and are now holding excess inventory of modules that are being undercut by cheaper newly-manufactured ones, placing themselves at risk of acquisition. Western wind turbine manufacturers are struggling with eroded margins driven by cost inflation and an R&D race to produce larger turbines, combined with an increasing competition from Chinese vendors. Consolidation in the clean technology industry is likely to foster a manufacturing base capable of operating more comfortably with thinner margins. Fossil fuel producers are coming off a period of near record margins, and several who have banked these profits and bought back shares are leveraging their balance sheets to acquire productive assets at a lower cost than what it would take to develop them internally (i.e., ExxonMobil and Chevron acquiring Pioneer Natural Resources and Hess, respectively). Conditions remain ripe for further consolidation in fossil fuels.

A make-or-break year for hydrogen?

Perhaps no aspect of the energy transition has received more attention than hydrogen over the past year. The US, UK, Netherlands, Germany, Denmark, Portugal, Australia, South Korea, and India have all announced supply-side subsidy schemes, with the EU, UK, Japan and South Korea also putting low-carbon hydrogen production targets in place. Bullish projections of future hydrogen demand have led to nearly 100 million mt of announced low-carbon hydrogen production capacity in various stages of the development pipeline. However, the industry is encountering sizeable cost increases, with required capital expenditure estimates going up by 40-50%. While some of the cost inflation may be transitory, electrolyser projects tend to be highly complex, bespoke, and are proving far harder to construct than initially anticipated. Capacity is increasing but the market is looking for 10-15 large final investment decisions (FIDs) in 2024 to give confidence that momentum can be maintained. Also under scrutiny will be the results of European hydrogen auctions. Bids significantly below ceiling prices will be evidence of confidence in the market and a tolerance on the part of developers to accept price and development risk. Bids at or close to the ceiling will suggest the opposite and could suggest that hydrogen supply may grow more slowly than anticipated.

Surpluses in critical metals are coming, but 2024 may be the last year of 'low' prices.

Battery metals prices surged in 2022 on rapid growth in demand for lithium, cobalt, and nickel. But demand has since moderated due to the global economic slowdown. A significant response on the supply side has already cooled prices, by as much as 50%. Lithium supply has risen more sharply in 2023, boosted by recent project startups notably in Latin America, nickel supply is surging from Indonesia and China and the flow of cobalt exports from the Democratic Republic of the Congo (DRC) has also increased. However, due to continued large increases in demand for batteries and potential instability in the DRC, these surpluses will likely fade. Due to the long-lead nature of mining development, another period of tightness is expected from 2025, with copper – the key metal for electrification - expected to see prices moving sharply higher over the medium-to-long term amid the emergence of significant market deficits for both raw material (concentrate) and refined products.

The geopolitics of energy and climate are entering a new phase.

Using energy as leverage in geopolitical affairs has a long and storied history, most recently in Russia's attempt to weaponise its energy supply in the invasion of Ukraine. While Europe has so far managed to balance supply and demand for oil and without too large of a disruption, the geopolitical landscape has likely been permanently altered. Without Europe as an offtaker, Russia is now extremely dependent on China, shifting the balance of power in negotiations regarding the development of the Power of Siberia 2 pipeline in Beijing's favour. China is also bolstering its global influence utilising its "Belt and Road Initiative" to supply both domestically-produced renewables and project finance to developing countries. China is not alone in using clean energy as leverage in international trade, as potential trading partners scramble to qualify for use under the US Inflation Reduction Act. Europe is eyeing protections to its domestic industry from trade and will unveil the specifics of its carbon border adjustment mechanism in 2024 as well as add shipping into the EU Emissions Trading Scheme. Both measures will effectively project European carbon pricing policy across the globe, with EU ETS prices set to rise to over €90 per metric ton on average in 2024.

Elections are a wildcard.

In 2024, 78 elections are scheduled across the world, over half of which will choose a new president. Over 2 billion people are expected to go to the polls. While perhaps not unprecedented, such a concentration of political risk into one single year is certainly historic. Attention naturally falls to the US, where any return of a Republican president to the helm of the worlds' largest economy could threaten to undo the provisions of the IRA, extract the US from participation in the Paris Agreement once again and reshape relations with trading partners. Elections to the European Parliament in June, as well as polls in individual European countries through the year will indicate whether or not the populist swing observed in some states in 2023 will be maintained. India's next general election will be held mid-year and votes will also take place in Indonesia, Mexico, and South Africa. Amid the emergence of more assertive nations in the Southern Hemisphere, which are seeking to match geopolitical influence with growing economic heft, the election year of 2024 could further reorder what is already a fluid and disjointed world.

A new wave of consolidation in clean tech; extended wave for fossil fuels

The unwinding of two years of polysilicon supply constraints has resulted in lower solar project costs and potentially wider margins for developers. As a result of this shift, some companies mistimed the cycle and are now holding excess inventory of modules that are being undercut by cheaper newly-manufactured ones, placing themselves at risk of acquisition. Western wind turbine manufacturers are struggling with eroded margins driven by cost inflation and an R&D race to produce larger turbines, combined with an increasing competition from Chinese vendors. Consolidation in the clean technology industry is likely to foster a manufacturing base capable of operating more comfortably with thinner margins. Fossil fuel producers are coming off a period of near record margins, and several who have banked these profits and bought back shares are leveraging their balance sheets to acquire productive assets at a lower cost than what it would take to develop them internally (i.e., ExxonMobil and Chevron acquiring Pioneer Natural Resources and Hess, respectively). Conditions remain ripe for further consolidation in fossil fuels.

A make-or-break year for hydrogen?

Perhaps no aspect of the energy transition has received more attention than hydrogen over the past year. The US, UK, Netherlands, Germany, Denmark, Portugal, Australia, South Korea, and India have all announced supply-side subsidy schemes, with the EU, UK, Japan and South Korea also putting low-carbon hydrogen production targets in place. Bullish projections of future hydrogen demand have led to nearly 100 million mt of announced low-carbon hydrogen production capacity in various stages of the development pipeline. However, the industry is encountering sizeable cost increases, with required capital expenditure estimates going up by 40-50%. While some of the cost inflation may be transitory, electrolyser projects tend to be highly complex, bespoke, and are proving far harder to construct than initially anticipated. Capacity is increasing but the market is looking for 10-15 large final investment decisions (FIDs) in 2024 to give confidence that momentum can be maintained. Also under scrutiny will be the results of European hydrogen auctions. Bids significantly below ceiling prices will be evidence of confidence in the market and a tolerance on the part of developers to accept price and development risk. Bids at or close to the ceiling will suggest the opposite and could suggest that hydrogen supply may grow more slowly than anticipated.

Surpluses in critical metals are coming, but 2024 may be the last year of 'low' prices

Battery metals prices surged in 2022 on rapid growth in demand for lithium, cobalt, and nickel. But demand has since moderated due to the global economic slowdown. A significant response on the supply side has already cooled prices, by as much as 50%. Lithium supply has risen more sharply in 2023, boosted by recent project startups notably in Latin America, nickel supply is surging from Indonesia and China and the flow of cobalt exports from the Democratic Republic of the Congo (DRC) has also increased. However, due to continued large increases in demand for batteries and potential instability in the DRC, these surpluses will likely fade. Due to the long-lead nature of mining development, another period of tightness is expected from 2025, with copper – the key metal for electrification - expected to see prices moving sharply higher over the medium-to-long term amid the emergence of significant market deficits for both raw material (concentrate) and refined products.

The geopolitics of energy and climate are entering a new phase

Using energy as leverage in geopolitical affairs has a long and storied history, most recently in Russia's attempt to weaponise its energy supply in the invasion of Ukraine. While Europe has so far managed to balance supply and demand for oil and without too large of a disruption, the geopolitical landscape has likely been permanently altered. Without Europe as an offtaker, Russia is now extremely dependent on China, shifting the balance of power in negotiations regarding the development of the Power of Siberia 2 pipeline in Beijing's favour. China is also bolstering its global influence utilising its "Belt and Road Initiative" to supply both domestically-produced renewables and project finance to developing countries. China is not alone in using clean energy as leverage in international trade, as potential trading partners scramble to qualify for use under the US Inflation Reduction Act. Europe is eyeing protections to its domestic industry from trade and will unveil the specifics of its carbon border adjustment mechanism in 2024 as well as add shipping into the EU Emissions Trading Scheme. Both measures will effectively project European carbon pricing policy across the globe, with EU ETS prices set to rise to over €90 per metric ton on average in 2024.

Elections are a wildcard

In 2024, 78 elections are scheduled across the world, over half of which will choose a new president. Over two billion people are expected to go to the polls. While perhaps not unprecedented, such a concentration of political risk into one single year is certainly historic. Attention naturally falls to the US, where any return of a Republican president to the helm of the worlds' largest economy could threaten to undo the provisions of the IRA, extract the US from participation in the Paris Agreement once again and reshape relations with trading partners. Elections to the European Parliament in June, as well as polls in individual European countries through the year, will indicate whether or not the populist swing observed in some states in 2023 will be maintained. India's next general election will be held mid-year and votes will also take place in Indonesia, Mexico, and South Africa. Amid the emergence of more assertive nations in the Southern Hemisphere, which are seeking to match geopolitical influence with growing economic heft, the election year of 2024 could further reorder what is already a fluid and disjointed world.